There’s broadly two types of student loan in England within the mainstream Student Loan Company constellation.

Undergraduate tuition fee loans constitute one type all on their own – it’s money that (as a student) you never see. The tuition fee loans are the closest we get to a graduate tax: you pay it (once you earn more than minimum wage) right up to the end of your working life if you are on Plan 5 (with early remission only available if you become unable to work or, randomly, get a very well paid job).

All the other major loans – postgraduate and doctoral loans, maintenance loans… – show up in your student bank account. They represent capital that can be used to fund the job of being a student (with loans above undergraduate level also being available to pay fees if needed). The amount available is means tested – based either on your own income (or that of your parents for undergraduates) – the amount you borrow doesn’t affect your repayments as a graduate (everyone pays nine per cent), just the length of time you repay given the higher total amount.

It’s a bit of a bold split given the rich panoply of SLC products – but it is one to keep in your head for the purposes. Either the money ends up in your account (and you can spend it on rent or food and such), or it doesn’t.

Cossy livs and debt

In the 2023-24 academic year, 6.7 per cent of full time undergraduates accessing the SLC system took out only a tuition fee loan. This is the highest proportion since 2015-16, and very much not what you would expect to see during a cost of living crisis. We see declines too in the take up of master’s and doctorate loans (in fact a link to the declining number of UK domiciled doctoral and master’s students) both multi-year trends.

Undergraduate maintenance loans are a slightly different beast as they have a negative relationship with overall levels of poverty among the parents of university-age young people. In other words, if more people have very low earnings, the state will take up a larger proportion of the cost of supporting their student offspring. Here, things look a little more like we would expect – the amount paid out in UG maintenance loans in 2023-24 was the highest on record, and grew much faster than the number of students in receipt of it.

Among those undergraduates who did take out a maintenance loan, the average amount awarded rose – to £7,460 in 2022-23. But that is just a 2.5 per cent rise on the average amount in 2021-22 – so in real terms the average support paid out per student fell. A part of this problem can be laid squarely at the door of the government – there was a derisory 1.8 per cent increase in the maximum available amount, and a failure to uprate the minimum level means even those households with one earner on minimum wage are expected to contribute to student living costs. You’d also expect the rise in (very well off, usually) students not bothering with maintenance loans to push the average amount per student up.

It may well be time to start asking if the overall attractiveness of the maintenance (into the bank) loan offer is falling – with the changes to repayment terms, the stackability of multiple UG and PG loans, and poor overall understanding of the loan system contributing to a reluctance to use the available support. Certainly, if the aim of the postgraduate loan system is to increase the number of young people taking qualifications at level 7 and above it does not appear to be working.

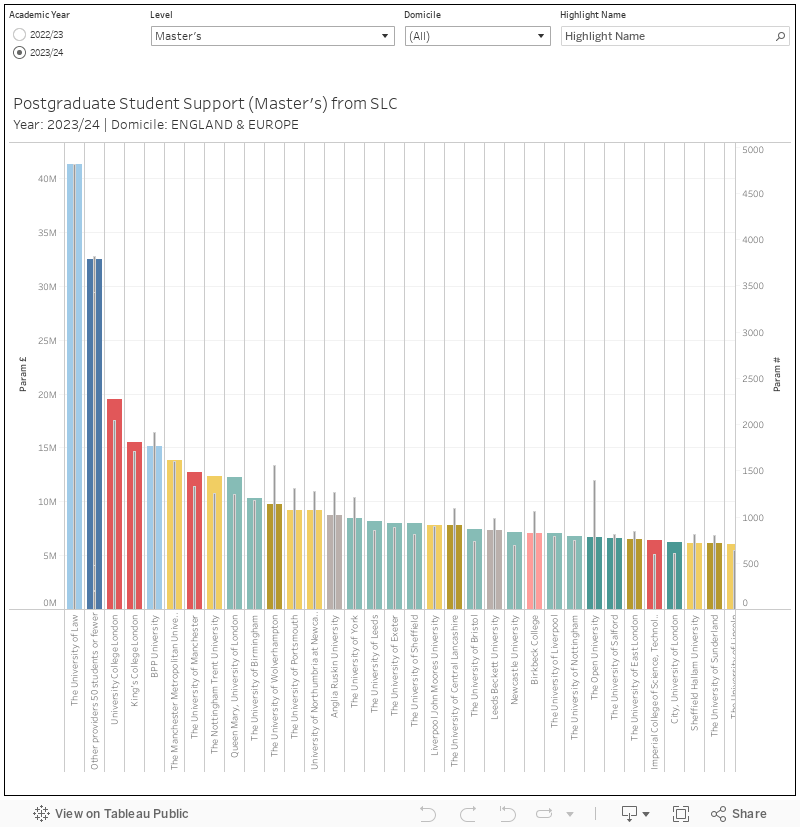

More about postgraduate loans

Everyone from Skills England down has highlighted a need for more people with postgraduate skills in the workforce. The policy intention appears to be that we train our own population, rather than relying (as we have in the past) on immigration. And as we have a load of world class universities you’d think that we’d be set. Wouldn’t you?

Well. The largest provider, numerically, of postgraduate loan backed level 7 provision is the University of Law. Whereas I’m sure these are decent professional development courses for early career lawyers looking to specialise, and there is some business-related provision in the mix too, I want to gently pose the question as to whether we as a nation want to spend twice as much supporting students here than at, say, UCL.

Switching the filter to look at doctoral loans we see another surprising facet – by some margin there are more students at smaller providers (with less than 50 peers) taking out loans to do doctoral work than at any single institution. There’s quite a few well-known providers in Wales, Scotland, and Northern Ireland mixed in here – and I imagine a number of smaller, world class, providers in here too. But if your image was of these loans supporting UK students at our more famous institutions you are wrong.

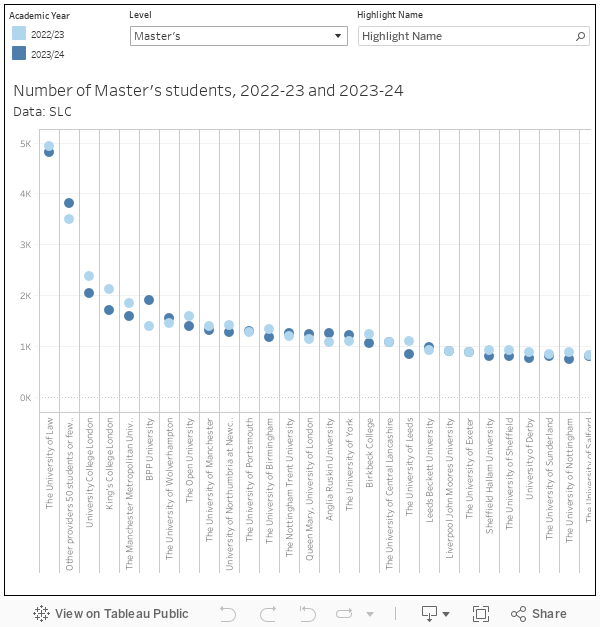

This data also gives us a first look at postgraduate student numbers in comparison to the year before. It’s necessarily a partial picture – as we’ve discussed, PG loans aren’t the most popular of products and many UK students manage without – but you can see who is expanding and who is contracting in this marketplace.

And where are the notable areas of growth for loan-backed UK students at master’s level? BPP, Chichester, Bolton, and those smaller providers. The biggest decline is at more traditional providers: UCL, King’s, Leeds. Postgraduate study – especially in the loan-backed form that would be more accessible to non-traditional students – doesn’t look like you may have expected. Doctoral loan uptake, too, is at a low ebb: with only Northampton, South Bank, West London, and the University of the Arts showing meaningful year on year growth.

Are more traditional postgraduate providers stepping away from the non-scholarship UK postgraduate market? Are other providers offering innovative opportunities or capitalising on unmet demand? We don’t have the answers in this data, but I hope someone at OfS has an answer.

Don’t forget about the undergraduates

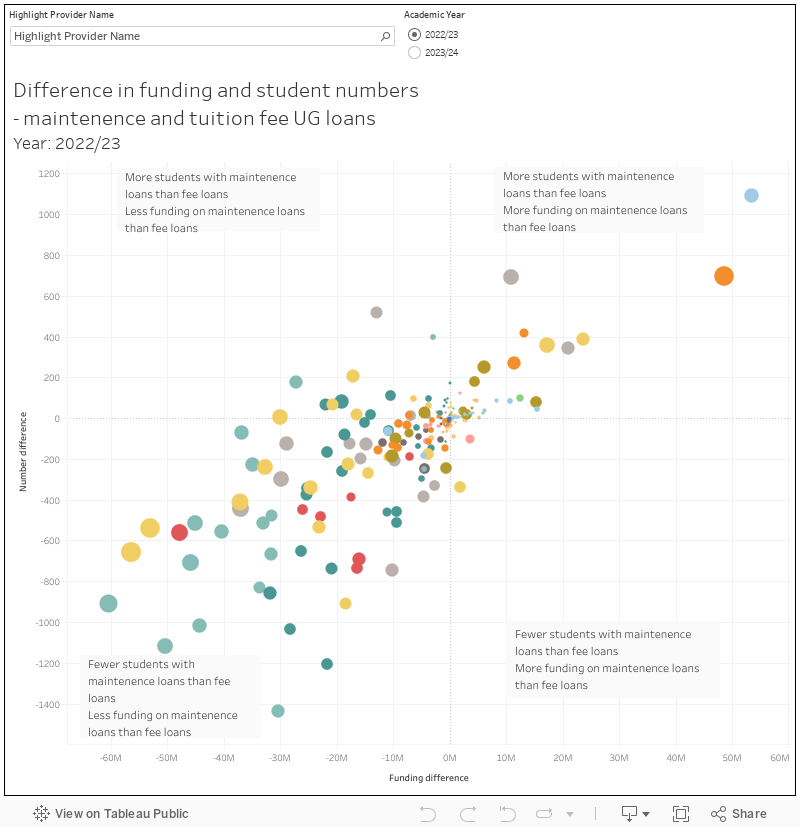

Another item on the regulatory to-do list might be to solve a conundrum I have presented on the site before. Why do a small group of providers have more students taking out maintenance loans (at a higher value) than tuition fee loans?

This chart shows (on the vertical axis) the difference between the number of students with undergraduate maintenance loans and UG fee loans, and (on the horizontal axis) the difference in pounds between the UG maintenance and UG fee loans taken out by students at that provider. You would expect to see a number of well-off students taking out only fee loans, and you’d expect to not see a smaller number of students taking out no loans at all for religious reasons – I’d reckon most of that 6.9 per cent I noted above.

At providers that primarily cater to students from disadvantaged backgrounds you might expect the value of maintenance loans to be higher than the value of fee loans. But I’m not sure under what circumstances a student would take out a maintenance loan and not a fee loan, and I am particularly unsure when you might expect the total value of maintenance loans to be higher than the total number of fee loans. The only thing I can find to connect the providers at the extreme top right of the chart is that most have recently seen an expansion of franchised provision.

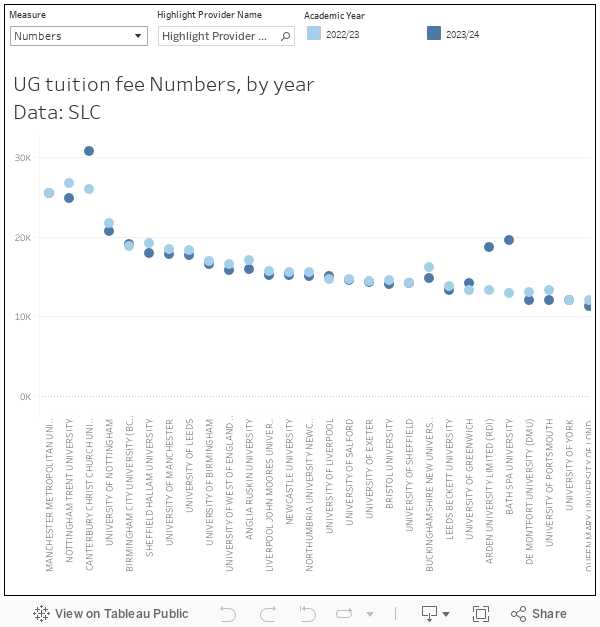

This release also gives us the first look at 2023-24 UK student numbers (as opposed to placed applicants) at undergraduate level. The stories here are more familiar – you can see the impacts of the growth of franchise and partnership provision at some providers, often at the expense of fee income (toggle between numbers and income at the top left)